Yes, bike insurance covers theft outside your house provided you have a Comprehensive or Own-Damage policy and the bike was properly locked. You will be paid the IDV (Insured Declared Value) of the bike. To get the full original price back, you must have the Return to Invoice add-on. Total claim settlement usually requires a 60–90 day wait for the police Non-Traceable report.

You walk out your front gate, helmet in hand, only to find an empty patch of pavement where your scooter or bike stood just hours ago. It is a sinking feeling that thousands of Indian vehicle owners experience every year. In cities like Delhi or Bengaluru, bike theft isn't just a possibility; it’s a statistical reality. Most riders assume that because they pay their premiums on time, the insurance company will simply hand over a cheque for a new bike. However, the transition from a stolen vehicle to a settled claim is rarely that linear. Whether your policy covers a bike parked on a public street versus a locked driveway depends entirely on the "fine print" regarding negligence and the type of cover you purchased.

By the end of this guide, you will know exactly how to bridge the gap between a total loss and a successful payout, ensuring you don't lose both your bike and your money.

So, Does Your Policy Actually Include Bike Theft Coverage?

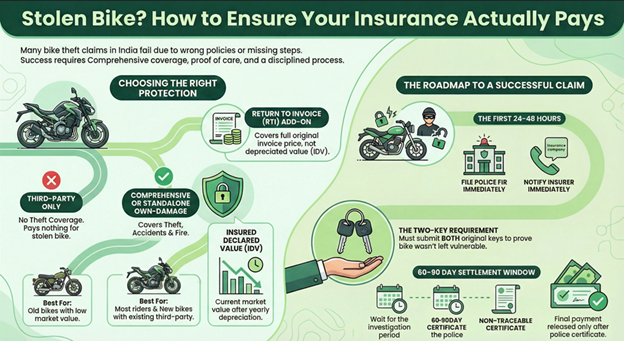

Not all insurance is created equal in the eyes of the law. In India, the Motor Vehicles Act makes Third-Party insurance mandatory, but this specific policy is designed to protect others, not you. If you only have third-party cover, your insurer will not pay a single rupee if your bike is stolen from outside your house or anywhere else.

To get protection against theft, you must buy bike insurance that is either a Standalone Own-Damage policy or a Comprehensive policy. These are the only frameworks that recognize theft as a Total Loss event. Under these plans, the insurer agrees to compensate you based on the Insured Declared Value (IDV) of the vehicle.

Think of it this way: the government forces you to buy protection for the stranger you might hit, but you must choose to buy protection for your own wallet.

Identifying Your Coverage Type

|

Policy Type |

Theft Coverage Included? |

Best For |

|

Third-Party Only |

No |

Old bikes with very low market value. |

|

Standalone Own-Damage |

Yes |

New bikes where you already have a multi-year third-party cover. |

|

Comprehensive |

Yes |

Most riders; covers accidents, fire, theft and third-party. |

Note: Coverage is subject to the terms and conditions of the specific policy document issued by the insurer.

When "Outside Your House" Becomes a Legal Gray Area

Here is what most people miss: the location of the theft matters less than the intent of care. Indian insurers look for signs of negligence. If you left your bike outside your house with the keys in the ignition, the insurer will likely reject your claim under the reasonable care clause.

If the bike was locked and parked in a spot where you usually keep it (even if that spot is a public road) the theft is generally covered. However, the burden of proof lies with you. You must prove that you took adequate precautions. This is why having a FIR (First Information Report) that explicitly mentions the bike was locked is non-negotiable.

Why You Should Purchase Bike Insurance with Return to Invoice (RTI)

When you purchase bike insurance, the standard payout for theft is the IDV. The IDV is the current market value of your bike after accounting for depreciation. If you bought a bike for Rs. 1,20,000 two years ago, your IDV might only be Rs. 90,000 today. If it gets stolen, you lose Rs. 30,000 and the cost of new registration and taxes.

That’s where the Return to Invoice (RTI) add-on becomes a lifesaver. This specific add-on ensures that in the event of theft, it covers the gap between IDV and invoice value, subject to policy terms, eligibility and limits defined by the insurer. It effectively ignores depreciation. For anyone owning a bike less than three years old, this is the most critical decision you can make during the purchase.

Step-by-Step: The Anatomy of a Theft Claim in India

If the worst happens and your bike vanishes, the next 24 hours are critical. Any delay can give the insurer a reason to doubt the authenticity of your claim.

- File an FIR Immediately

Contact the nearest police station. An FIR must be filed and a copy (physical or digital, depending on state systems) must be submitted to the insurer as proof of theft. Ensure the police record the correct engine number and chassis number.

- Notify the Insurance Company

Call your insurer's helpline. Most companies require notification within 24 to 48 hours. They will provide a claim reference number which you must save.

- Inform the RTO

As part of the claim process, insurers require submission of RTO-related documents (such as Forms 28, 29, 30) to transfer ownership to the insurer. They will provide a Non-Traceable Certificate after a certain period (usually 30 to 90 days), which is the final document required to release your payment.

- Submit the Keys

This is the part that catches people off guard. Insurers typically require submission of available keys; missing keys may lead to additional investigation during claim assessment. If you cannot provide both, they may argue that you left a key in the bike, citing negligence.

Ready to secure your ride?

Don't wait for a missing bike morning to realize your coverage is insufficient. Compare the best comprehensive plans with theft protection today at SMC Insurance.

Essential Documents for a Seamless Claim Experience

Accuracy is the difference between a settled claim and a legal battle. Ensure you have the following documents ready in a digital folder:

- Original Policy Document: Proof of active coverage.

- FIR Copy: The primary legal evidence of the crime.

- Form 28, 29 and 30: These are RTO transfer forms you must sign to transfer the ownership of the stolen (non-existent) bike to the insurer.

- Final Police Report: Often called the Untraceable Report or v-summary, confirming the police could not find the vehicle.

- Original Keys: Both sets are mandatory.

Common Reasons Claims for Bike Theft Coverage are Rejected

Understanding the pitfalls helps you avoid them. Insurers in India are strictly regulated by the IRDAI, but they are also businesses that look for policy violations.

- Delay in Reporting: If you wait a week to file an FIR because you were busy, your claim is as good as dead.

- Negligence: Parking in a restricted zone or leaving the handle unlocked.

- Use for Commercial Purpose: If your personal bike was stolen while being used for a delivery job, the claim will be rejected unless you have a commercial policy.

- Modified Parts: If you added expensive alloys but didn't inform the insurer, you will only be paid for the stock parts.

Note:

- Installing ARAI-approved anti-theft devices can help reduce premiums and may support claim credibility.

- If the bike is under loan, the claim amount is first settled with the financer and any remaining amount is paid to the policyholder.

- Many insurers now allow digital claim intimation and document submission through apps or websites.

Must Read Guide From SMCInsurance

Wrapping Up,

Theft is an unpredictable reality, but your financial recovery doesn't have to be. To ensure you are protected when your bike is parked outside your house, you must move beyond basic third-party plans. Buy bike insurance with a high IDV or a Return to Invoice add-on to bridge the gap between what you paid and what the insurer offers. Remember, the reasonable care you take today, like locking the handle, keeping both keys safe and parking in well-lit areas, is the primary evidence that will win your claim tomorrow.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

If you lost your keys and then the bike was stolen, the claim becomes very difficult. Insurers require both original keys to prove you weren't negligent. If you lose a key, you should immediately inform the insurer and get the lock-set replaced. If you didn't do this, the claim for bike theft coverage may be rejected.

Yes, bike insurance provides pan-India coverage. As long as you have a comprehensive policy, the location within India does not matter. However, you must file the FIR in the local police station where the theft occurred and notify your base RTO later.

Without add-ons, you receive the Insured Declared Value (IDV) minus the compulsory deductible (for two-wheelers, typically Rs. 100 for up to 150cc and Rs. 200 for above 150cc, though exact values are defined in policy terms). The IDV is calculated as: Manufacturer’s listed selling price – Depreciation. If you purchase bike insurance with a 'Return to Invoice' cover, you get the full amount mentioned on your original bill.

The process is slower than accident claims. It usually takes 60 to 90 days. This is because the insurer must wait for the police to issue a Non-Traceable Certificate, which confirms the bike cannot be found. Only after this document is submitted can the final payout be processed.

Yes, you will lose your No Claim Bonus (NCB). The NCB can offer a discount of up to 50% on your own-damage premium if you haven't made a claim in five years. When you claim for theft, this discount resets to zero for the following year.