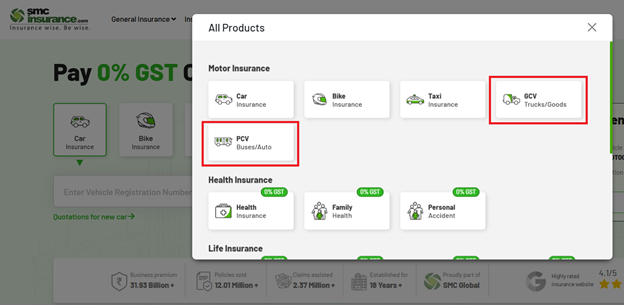

Visit the SMC Insurance Brokers Official website and click on the “View All” option..

100% Privacy

Zero Spam

Network

30+ Reliable Insurers

Legacy

20+ Years & Counting

Highly rated insurance website

4.1/5

Plans start at Just ₹49.24/day

You might have invested in vehicles be it a cab, a mini-truck, or a school bus to generate income for yourself. These vehicles become important revenue-generating assets for you.

Like any other revenue-generating asset, you need to financially protect these vehicles to avoid business disruption due to any kind of accidental damage or liability due to damage of any third party person or property on the road.

What’s more, you are legally required to buy an insurance cover for your vehicle. If you don’t own one, you can face legal repercussions like fines, etc.

In this article, we’ll discuss what insurance for commercial vehicles is and how it works.

A commercial vehicle is any vehicle used for business purposes to transport passengers or goods. These vehicles operate to earn income or support business activities. Many of them also carry heavier loads compared to private vehicles. Common examples include:

In India, commercial vehicles often have higher gross vehicle weight and require commercial registration.

Commercial vehicle insurance is a motor insurance policy designed for vehicles used for business activities. The policy provides financial protection if the vehicle is damaged, stolen, or involved in an accident. It can also cover legal liabilities if the vehicle causes injury to another person or damage to property. Commercial vehicle insurance typically covers:

Having commercial insurance helps businesses manage unexpected repair costs and legal compensation claims.

Several insurers offer policies specifically designed for goods carriers, passenger vehicles and specialized commercial vehicles. These plans typically provide third-party liability cover and optional comprehensive coverage for damage to the insured vehicle. Below are some of the widely known insurers offering commercial vehicle insurance in India in 2026:

| Insurance Provider | Key Strengths | Suitable For |

|---|---|---|

| ICICI Lombard General Insurance |

|

|

| Bajaj General Insurance |

|

|

| Go Digit General Insurance |

|

|

| IndusInd General Insurance |

|

|

| SBI General Insurance |

|

|

| New India Assurance Company Limited |

|

|

| Shriram General Insurance |

|

|

| United India Insurance Company Limited |

|

|

Note: Our best plan selections are based on: Industry recognition, customer experience metrics, insurer comparisons, features and ratings (in no-specific order).

Here are 3 important reasons behind buying insurance for commercial vehicles -

A commercial vehicle is part of your business family. It is always on the road, sometimes even for 24 hours. Its frequency of travel is higher than private vehicles, which in turn, exposes it to a greater risk of damage. Any damage to a commercial vehicle puts the vehicle off-road, thus having an impact also on the business and its revenues. It is hence important to cover commercial vehicles with insurance, It financially covers your business against any losses due to major damage to your vehicle.

Commercial vehicles run for long hours and across different kinds of routes, areas, and cities. These vehicles are often driven by paid drivers who may cause injury to someone on the road, or ram the vehicle to an expensive property/asset. As per law, your business will be liable to pay damages for injury or damage based on liability awarded by the court of law. Such losses may severely affect your business and its profitability. Through third-party insurance, you are covered for unlimited liability on death/injuries and liability up to Rs. 7.5 lakhs in case of damage to property.

Besides the liability explained above, It is also compulsory under the law that every vehicle (be it commercial or private) on the road must have at least third-party insurance. If you don’t comply with these rules, you can face legal repercussions like fines, etc. that again be an unnecessary loss for your business.

| Liability Type | Coverage Limit |

|---|---|

| Third-party injury or death |

|

| Third-party property damage |

|

Commercial vehicle insurance policies are broadly divided into two main categories. The difference between them lies in the level of protection they offer. While one focuses only on legal liability, the other provides wider protection that also covers damage to the vehicle itself. Choosing the right type of policy depends on how the vehicle is used, the value of the vehicle and the level of financial protection the owner wants.

Third-party insurance is the most basic form of motor insurance and is mandatory under Indian law. According to the Motor Vehicles Act, every vehicle operating on public roads must carry at least third-party liability insurance.

This policy protects the vehicle owner against legal liability if the insured vehicle causes injury, death, or property damage to another person. For instance, if a commercial truck collides with another vehicle or damages public property, the insurer pays compensation to the affected third party as per the decision of the Motor Accident Claims Tribunal.

However, third-party insurance does not cover damage to the insured commercial vehicle. Any repair expenses for the vehicle must be borne by the owner. Third-party insurance mainly helps vehicle owners comply with legal requirements and protects them from major liability claims.

Comprehensive commercial vehicle insurance offers broader protection compared to third-party insurance. In addition to covering third-party liability, this policy also protects the insured vehicle against various risks. A comprehensive policy generally covers damage caused by accidents, fire, theft, vandalism and natural disasters such as floods, cyclones, earthquakes and landslides. It also provides financial protection if the vehicle is completely lost or stolen.

Because commercial vehicles often operate continuously and travel long distances, the chances of damage are higher. Comprehensive insurance helps vehicle owners avoid large repair costs and business disruption when such events occur. Another advantage of comprehensive policies is the option to include add-on covers. These optional covers allow vehicle owners to expand their policy protection. Add-ons such as zero depreciation cover, engine protection and roadside assistance can be added depending on the needs of the vehicle and business.

Below is a clear overview of the common inclusions and exclusions found in most commercial vehicle insurance policies in India.

A comprehensive commercial vehicle insurance policy usually covers losses or damages caused by a range of unexpected events. These protections ensure that the vehicle owner does not have to bear the entire financial burden when such incidents occur.

|

|

|

|

|

|

|

|

|

|

|

|

Despite offering wide protection, commercial vehicle insurance policies do not cover every possible situation. Certain events and conditions are excluded from the policy.

Here is why owning insurance for commercial vehicles is beneficial -

Here’s a table that demonstrates how insurance premiums vary across different commercial vehicle types -

| Vehicle Category | Third-Party Premium (Approx.) |

|---|---|

|

|

|

|

|

|

|

|

|

|

|

|

Although the specific policy features differ from one insurer to another, most commercial vehicle insurance plans offer similar core benefits.

Let's face it, your car is an income generator. Here's why you shouldn't leave it uninsured.

It's not hard to figure out how much your commercial car insurance will cost; there is a method to it.

Car Insurance Premium = Own Damage Premium – (No claim bonus + discounts) + Third Party Liability

Insurance companies provide a convenient premium calculator: simply enter the vehicle's make, model, registration state, manufacture year, and your personal details. When you click "calculate," you'll get an estimated premium for both new and used vehicles, be it comprehensive or third-party.

Insurance companies calculate premiums using several factors:

The insurance premium for your commercial vehicle is determined by a variety of factors. Here are the details:

This is basically the current market worth of your car. A higher IDV provides more coverage, but at a higher cost.

Larger engines mean more danger, which means higher insurance rates. That's just basic maths.

The cost of third-party insurance is lower. However, adding options like zero-depreciation, roadside assistance, or return-to-invoice to a comprehensive plan makes you sleep better, but it comes with a cost.

Your premium will go down if you choose a higher deductible, but keep in mind that you will have to pay more out of pocket in the event of a claim.

Over a five-year period, you can receive a savings of up to 50% if you remain claim-free. However, one claim may offset that benefit.

High-risk areas or crowded city streets? You can expect premiums to reflect this. Also, public carriers are subject to higher charges than private ones.

It may surprise you to learn that your driving record and licence history also matter. Lower risk equals lower rates.

Although they might not be eligible for as many add-ons, older cars have lower insurance costs.

Prior to clicking "buy," pause and consider this:

Add-ons are optional covers that can be added to a comprehensive commercial vehicle insurance policy to enhance protection. These covers help extend the scope of the basic policy and protect the vehicle against additional risks that are not included in standard coverage. Below are some commonly available add-ons in commercial vehicle insurance:

| Add-on Cover | What it Covers |

|---|---|

| Zero Depreciation Cover |

|

| Engine Protection Cover |

|

| Roadside Assistance |

|

| Consumables Cover |

|

| Return to Invoice Cover |

|

| Loss of Income Cover |

|

Compared to other options, SMC Insurance is far better and offers many significant benefits:

Getting commercial vehicle insurance through SMC’s website is quick and straightforward:

From the available options, select if your vehicle is GCV (Goods Carrying Vehicle) or PCV (Passenger Carrying Vehicle)

Once chosen, you will be taken to the respective page. You can use the on-screen widget and enter your vehicle number and click on “View Quotes”. This will directly take you to the commercial insurance buying process of SMC Insurance.

Fill in the required vehicle details. This includes vehicle category, brand, model, RTO location, and how long you want the policy to last.

Review quotes from multiple insurance partners and compare pricing and benefits side by side.

Customize your policy by adding optional protections like roadside support or engine cover, based on your needs.

Complete the payment online. Your policy documents are sent to your email soon after payment confirmation.

Download the policy from the SMC app or your email. Check all details carefully, then you’re set to drive with coverage in place.

With SMC, submitting a claim is easy:

When things go wrong on the road, commercial vehicle insurance is your safety net. The correct coverage keeps your wheels (and revenue) veering, whether it's a minor collision or a serious accident. Consider it an investment in mental well-being rather than merely security. With support like SMC Insurance, you can future-proof your business in addition to insuring your car with features like customised add-ons, round-the-clock assistance, and easy digital procedures. Thus, don't wait for problems to arise. With the right policies in place, you can grow your business with assurance, security, and complete authority.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

(Showing Newest to Oldest)

Simple Process

The company is wonderful insurance platform providing multiple policies under 1 roof. Experience in purchasing the policy is very good. Experts guides you very well

Easy Renewal process

The process to renew my 2-wheeler policy is indeed very quick and easy. Got it done in just 10 minutes. Thanks.

Quick Response

I thought let me renew my two wheeler policy with SMC and see the experience. The experience was good and simple, the only gap which I felt was that the details of the vehicle did not come up after mentioning the vehicle number.

Yes, you can easily purchase it online through platforms like SMC Insurance. Just enter your vehicle details, compare quotes, pick the plan, pay, and receive your policy instantly.

Yes, at least third-party insurance is legally required for all commercial vehicles on Indian roads.

No, you’ll need to purchase a separate commercial policy. Private insurance doesn't cover business use.

Yes, passenger and goods vehicles have different premium rates, coverage types, and regulatory norms due to their unique risk profiles.

You could face fines up to Rs. 2,000 and/or imprisonment. Plus, any accident-related liability could fall entirely on you.

Premiums vary based on vehicle type, engine capacity, usage, and location. For example, TP premium for a 7,500 kg goods vehicle is around Rs. 16,049/year.

You’re liable for all damages (your own and third-party); plus, you risk fines, legal issues, and business disruption.

It’s based on factors like vehicle type, engine capacity, IDV, location, usage, driver history, and selected add-ons.

Legally, yes. But if you want protection for your own vehicle too, opt for a comprehensive policy as it is smarter in the long run.

Yes, you can transfer the policy to the new owner with the insurer’s approval. Make sure to update ownership details.

It’s a reward for not making any claims in a policy year. You get a discount on your renewal premium, up to 50% over time.

Yes, if you’ve included personal accident cover or opted for specific employee protection add-ons.

Yes, passenger-carrying vehicles like cabs, taxis, and auto-rickshaws have tailored insurance plans to cover passenger-related risks.

Visit your insurer’s website or app (like SMC Insurance), enter your policy details, pay online, and you’ll receive a renewed policy instantly.

Only if you’ve opted for the engine protector add-on. Basic plans usually don’t cover engine or gearbox damage caused by waterlogging or oil leaks.

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

SMC Insurance Brokers Pvt. Ltd.

SMC Metro Mall, Near Pratap Nagar Metro Station, Pratap Nagar, New Delhi-110007

Registration No: 289, Registration Code No: IRDAI/DB-272/04/289, Valid till: 27/01/2029, License category: Composite Broker, CIN: U66000DL1995PTC172311

Insurance is the subject matter of solicitation.

Visitors are hereby informed that their information submitted on the website may be shared with insurers.

Product information is authentic and solely based on the information received from the Insurer.