IDV (Insured Declared Value) is the maximum amount an insurer pays if your car is stolen or damaged beyond repair. It equals your car's ex-showroom price minus age-based depreciation as fixed by IRDAI (ranging from 5% for cars under 6 months old to 50% for cars aged 4–5 years). For cars beyond 5 years, IDV is mutually agreed between insurer and policyholder. A higher IDV means a higher premium but greater claim protection. The right IDV should closely reflect your car's actual current market value, neither inflated nor deflated. Always verify your IDV at every renewal.

You renew your car insurance every year. You pay the premium. And somewhere in the policy document, there's a number called IDV — Insured Declared Value. Most people skip right past it. Then their car gets stolen or totalled and they discover it was that one number that decided how much they actually received. Not the premium they paid. Not the brand of the insurer. Just the IDV.

Understanding IDV in car insurance is not complicated. But getting it wrong (either too high or too low) has very real financial consequences. This article explains what IDV means, how it's calculated using IRDAI's official depreciation schedule, how it affects your premium and what you should actually do at renewal time.

What IDV in Car Insurance Actually Means

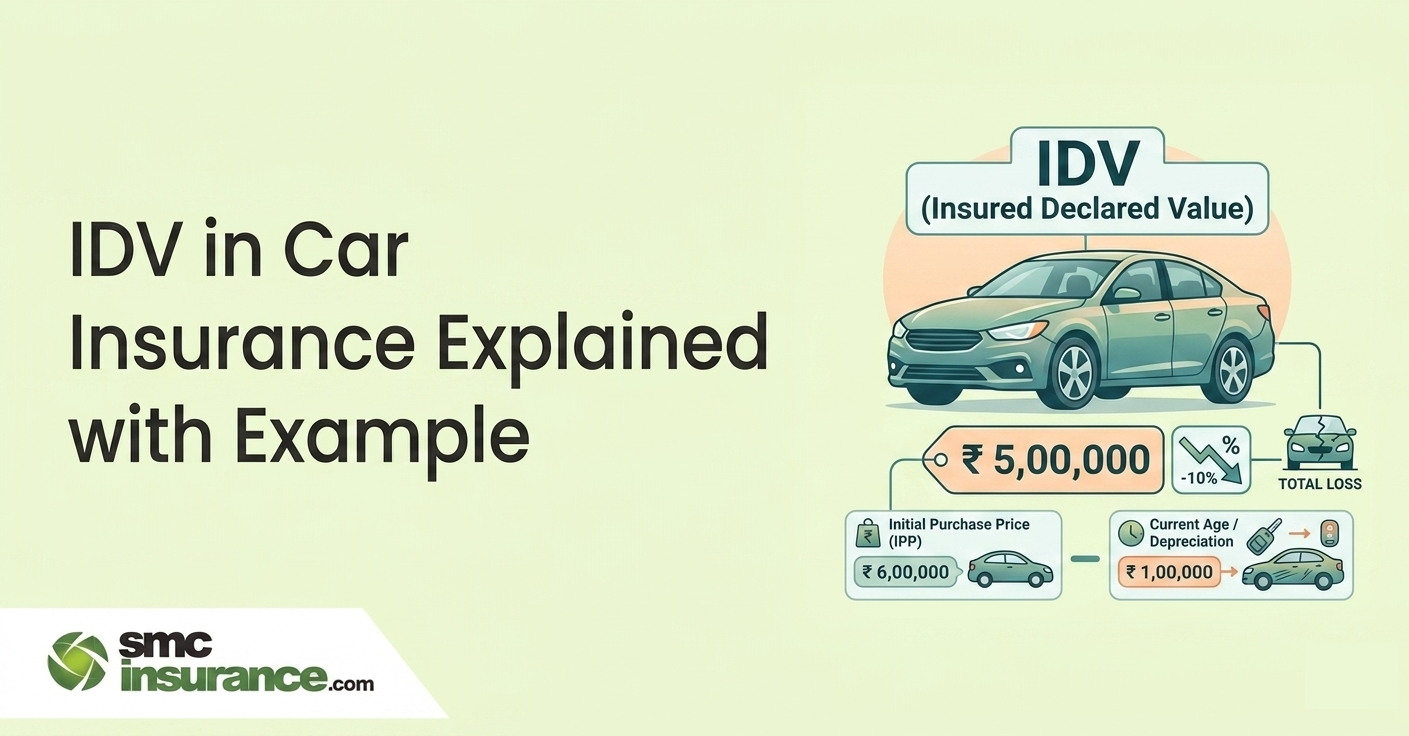

IDV stands for Insured Declared Value. It is the maximum amount your insurer will pay you if your car is stolen or damaged beyond repair - what the industry calls a total loss or constructive total loss (CTL).

IDV represents a standardised estimate of your car’s current market value, calculated using depreciation norms defined by IRDAI. It is not the price you paid at the showroom. It is not the on-road price. It is calculated based on the manufacturer’s listed selling price of the vehicle (excluding registration and insurance costs), adjusted for depreciation as per IRDAI guidelines.

The Official Definition from IRDAI

The Insurance Regulatory and Development Authority of India (IRDAI), which governs all general insurance in the country, defines IDV in the standard motor insurance policy wording as the "market value" of the vehicle for the purpose of total loss and constructive total loss claims. This value remains fixed during the policy period unless modified through an endorsement, meaning no further depreciation is applied during the policy period once the IDV is set.

A car is declared a constructive total loss when the cost of repair exceeds 75% of its IDV. In total loss or constructive total loss claims, the insurer pays the IDV. If the policyholder retains the salvage, its value is deducted from the payout.

What IDV Does Not Cover?

IDV is relevant only for comprehensive car insurance. If you hold only a third-party policy — which covers damage you cause to others — IDV does not apply. For partial damage claims (dents, broken windshields, minor accidents), the insurer pays actual repair costs, not the IDV. However, depreciation on parts replaced is still deducted in partial claims unless you have a zero-depreciation add-on.

How IDV Is Calculated: The IRDAI Depreciation Schedule

Every insurer in India uses the same depreciation schedule laid down by IRDAI to calculate IDV. Here's the formula:

IDV = Manufacturer's Listed Ex-Showroom Price − Depreciation Value

If your car has non-standard accessories (alloy wheels, upgraded music system, aftermarket additions), their declared value, subject to depreciation and acceptance by the insurer, is added separately to the IDV.

IRDAI's Official Age-Wise Depreciation Table for IDV

|

Age of the Vehicle |

Depreciation Rate for IDV |

|

Up to 6 months |

5% |

|

6 months to 1 year |

15% |

|

1 year to 2 years |

20% |

|

2 years to 3 years |

30% |

|

3 years to 4 years |

40% |

|

4 years to 5 years |

50% |

|

Above 5 years |

Mutual agreement between insurer and insured |

Source: IRDAI Standard Motor Insurance Policy Wording. For vehicles older than 5 years and discontinued models, IDV is determined by mutual agreement between the insurer and the policyholder — often based on market surveys or third-party valuation tools.

Worked Example: A 3-Year-Old Maruti Suzuki Baleno

Say you bought a Maruti Suzuki Baleno with an ex-showroom price of Rs. 8,00,000 three years ago. It is now in the 2-to-3-year age bracket, which attracts a 30% depreciation.

- Depreciation value: 30% of Rs. 8,00,000 = Rs. 2,40,000

- IDV = Rs. 8,00,000 − Rs. 2,40,000 = Rs. 5,60,000

If you have declared accessories worth Rs. 30,000 (with their own 30% depreciation applied):

- Accessories after depreciation: Rs. 30,000 − Rs. 9,000 = Rs. 21,000

- Total IDV = Rs. 5,60,000 + Rs. 21,000 = Rs. 5,81,000

This Rs. 5,81,000 is the ceiling on what your insurer pays if the car is stolen or written off. Not a rupee more.

How IDV Affects Your Car Insurance Premium?

This is where many policyholders make a mistake - deliberately!

Your car insurance own-damage (OD) premium is calculated as a percentage of IDV. The higher the IDV, the higher the premium. This leads some people to declare a lower IDV just to reduce what they pay annually. Saving Rs. 1,500–Rs. 2,500 on premium sounds reasonable until the car is totaled and the claim comes in far short of replacing it.

IDV vs. Premium

|

IDV Declared |

Approximate OD Premium (Illustrative) |

Claim Received on Total Loss |

|

Rs. 4,00,000 |

~Rs. 8,000–Rs. 10,000/year |

Up to Rs. 4,00,000 |

|

Rs. 5,00,000 |

~Rs. 10,000–Rs. 12,500/year |

Up to Rs. 5,00,000 |

|

Rs. 6,00,000 |

~Rs. 12,000–Rs. 15,000/year |

Up to Rs. 6,00,000 |

Note: OD premium rates vary by insurer, city, engine capacity, NCB (No Claim Bonus) and add-ons chosen. The above is illustrative, not a quote. Actual premiums must be verified with your insurer.

The Rs. 2,000 you save annually by undervaluing IDV can cost you Rs. 1,00,000 or more at claim time. That's not a trade-off; it's a trap.

Equally, inflating IDV beyond the actual market value doesn't help either; you'll pay a higher premium, but insurers may reassess the vehicle’s value at claim stage if the declared IDV is significantly inconsistent with its actual condition. For own-damage cover, insurers determine premiums based on multiple factors including IDV, vehicle age and claim history and may charge different rates for similar coverage as permitted under IRDAI guidelines.

The Right IDV: Neither Low Nor High

The ideal IDV is one that closely reflects your car's real current market value. For new cars up to 5 years old, the IRDAI depreciation schedule takes care of this automatically — just ensure your insurer is using the correct ex-showroom price for your vehicle's make, variant and city.

For cars older than 5 years, the IDV is negotiated. This is where you need to do some homework. Check used car platforms for your make, model and year to get a sense of actual resale value. Don't let the insurer default to the lowest number; don't push for an unrealistically high figure either.

When You Should Consider Adjusting IDV?

|

Situation |

What to Do |

|

Car is in excellent condition for its age |

Negotiate a slightly higher IDV with your insurer |

|

Car has high mileage, visible wear |

Accept standard or lower IDV to keep premium reasonable |

|

Car is more than 5 years old |

Compare market resale prices and fix IDV accordingly |

|

Car has aftermarket accessories |

Declare them separately; their depreciated value adds to IDV |

|

Switching insurers at renewal |

Confirm the new insurer uses the same ex-showroom reference price |

Note: Insisting on IDV significantly above actual market value will likely cause disputes at claim settlement. Insurers may assess actual market value independently during a total loss claim.

Not sure what IDV your car currently carries — or whether it's the right number? Comparing policies side-by-side before renewal makes sense. Visit SMC Insurance to check plans, compare IDV options and buy car insurance with the right coverage for your vehicle's current value.

IDV at Claim Time: What Actually Happens

Setting the right IDV is only half the picture. Understanding how it applies during a claim is the other half.

For total loss and theft claims: You receive IDV minus the compulsory deductible (typically Rs. 1,000 for cars up to 1,500cc and Rs. 2,000 for higher engine capacity vehicles, as per standard industry practice aligned with IRDAI guidelines) and minus salvage value if the wreck is retained by the insurer.

For partial damage claims: IDV is the upper cap — but the actual payout is the cost of repairs, subject to depreciation on replaced parts (unless you hold a zero-depreciation add-on). The insurer won't pay more than the IDV even for repairs, but in practice, partial claims rarely approach IDV.

CTL threshold: If repair costs exceed 75% of the IDV, the vehicle is declared a constructive total loss. At that point, the insurer pays you IDV minus salvage and the vehicle's Registration Certificate (RC) must be cancelled, as required under motor vehicle regulations, the Registration Certificate (RC) must be cancelled after settlement of a total loss claim.

Must-Read Guides From SMC

- Buy Car Insurance

- Best Car Insurance Company in India

- VIP Number Plate Price

- Check PUC Status Online

- Check Vehicle Details

- RTO Guide

- PUC for Modified Cars & Aftermarket Exhausts in India

- RC Transfer & Car Insurance Transfer Process

- Factors Affecting Car Insurance Policy Premium

- Features of a Car Insurance Policy

- Types of Car Insurance Policy

Summing Up,

IDV in car insurance is not a formality. It's the financial foundation of your own-damage coverage. Every claim scenario (theft, flood, accident write-off) resolves to this single number. The IRDAI has fixed clear depreciation rates to ensure uniformity across all insurers, but the responsibility of checking and confirming your IDV at each renewal falls on you.

Don't let renewal become a routine where you just click "renew" and move on. Spend two minutes confirming that your IDV matches your car's actual market value. If your car is older than 5 years, invest a little more time comparing resale prices before accepting whatever your insurer proposes. And if you've added accessories after purchase, declare them — their depreciated value increases your IDV and your claim protection. The right IDV costs you a fair premium and pays you a fair claim. That's the deal.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

IDV stands for Insured Declared Value. It is the maximum amount your insurer will pay you if your car is stolen or declared a total loss. It is calculated by deducting IRDAI-mandated depreciation from your car's ex-showroom price. IDV matters because it directly determines your claim payout and not what you paid for the car, not what it costs to replace it new, but the current assessed market value. Getting the IDV right at renewal ensures you're neither overpaying on premium nor underprotected at claim time.

For a car between 4 and 5 years old, IRDAI’s standard depreciation schedule applies a 50% rate. So if your car's ex-showroom price was Rs. 10,00,000, the IDV would be Rs. 10,00,000 minus 50%, which equals Rs. 5,00,000. Any declared accessories not included in the original manufacturer's price are also depreciated and added separately. This is the figure that appears in your policy schedule and determines your total loss claim ceiling.

Yes, to a limited extent. IRDAI permits some flexibility and insurers typically allow IDV to be set within a range around the calculated value. You can push for a slightly higher IDV if your car is exceptionally well-maintained. However, setting IDV significantly above market value is not advisable; at claim time, the actual payout is based on market value and disputes can arise. Setting it artificially low to save premium is equally inadvisable. The savings are minor and the financial gap at claim time can be significant.

For vehicles beyond 5 years of age, IRDAI does not prescribe a fixed depreciation rate. Instead, the IDV is determined by mutual agreement between the insurer and the policyholder. In practice, insurers may refer to used car valuations, third-party tools, or surveyor assessments. As a policyholder, you should check current resale prices for your make, model, year and city on established used car platforms before accepting the IDV your insurer proposes.

No, third-party insurance premiums are fixed by IRDAI based on vehicle type and engine capacity; they have no relation to IDV. IDV only affects own-damage (OD) premium in a comprehensive car insurance policy. If you hold only a third-party policy, IDV is irrelevant to your coverage, since third-party insurance does not cover damage to your own vehicle.

IDV is the base value used to calculate claim payouts. In standard comprehensive policies, depreciation is deducted on replaced parts during partial damage claims — meaning you bear a portion of the repair cost. A zero-depreciation add-on (also called nil-dep or bumper-to-bumper cover) waives this depreciation on parts, so the insurer pays the full cost of replacement parts without deductions. Zero-depreciation does not change your IDV; it changes how depreciation applies to parts during partial claims. Both concepts are important but serve different purposes.

Yes, since IDV is based on the current ex-showroom price of your model and your car's age-based depreciation, it changes every year. A policy renewed without checking can carry a stale IDV — either too high (leading to unnecessary premium) or too low (leading to a shortfall at claim time). Make it a habit to verify the IDV shown at renewal and cross-check it against the depreciation schedule before accepting the policy.