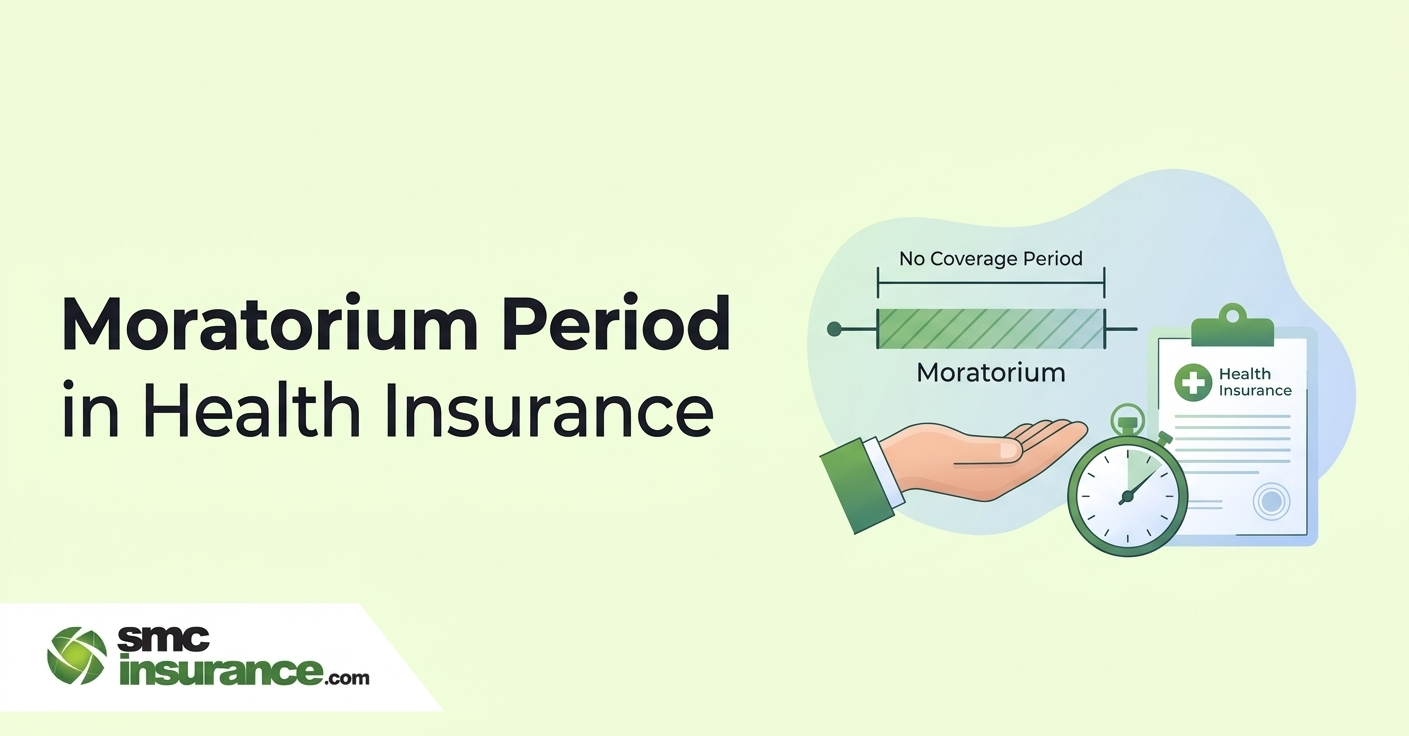

The moratorium period in health insurance is a 5-year continuous duration from the policy start date, as defined by the Insurance Regulatory and Development Authority of India (IRDAI). During this time, insurers can investigate claims for non-disclosure or misrepresentation. After completing 5 continuous years without a break, insurers cannot reject claims on these grounds, except in cases of proven fraud. This rule makes long-term health insurance policies more secure over time, provided they are renewed without interruption.

Ravi bought a health insurance policy at 32. Premium felt reasonable and coverage looked decent. He skimmed the document, nodded at the agent and moved on with life. Fast forward five years. A routine checkup turned serious. A surgery was advised. He filed a claim, confident everything was covered. That’s when the insurer pointed to a clause he barely remembered: the moratorium period.

Here’s the twist: because of how his policy was structured and renewed, certain disclosures and conditions still mattered even after years of paying premiums. That moment hits hard. You assume time has your back. Sometimes it does, sometimes it doesn’t.

The moratorium period in health insurance is one of those terms that sounds technical but quietly shapes how secure your policy really is. Get it right and your cover becomes stronger over time. Miss the nuance and you could face unpleasant surprises years later. By the end of this, you’ll know exactly how the moratorium period works in India, what changes after it ends and how to make sure it actually protects you.

What Is a Moratorium Period in Health Insurance?

Insurance contracts rely on trust. You disclose your health history. The insurer agrees to cover future risks. Now think about the problem insurers face. What if someone hides a pre-existing illness, buys a policy and claims a large amount after a few years?

That’s where the moratorium period in health insurance comes in. The Insurance Regulatory and Development Authority of India (IRDAI) defines this period as 5 continuous years from the policy start date. During this time, insurers can question claims or even deny them if they find non-disclosure or misrepresentation.

After those 5 years, something changes. Insurers cannot reject claims on the grounds of non-disclosure or misrepresentation (except in proven fraud cases). That’s the core protection.

Key Fact: After completing 5 continuous years under a health policy, insurers lose the right to reject claims for most non-disclosure issues, unless fraud is clearly proven. If the sum insured is increased later, the moratorium period applies separately to the enhanced portion from the date of increase.

How the Moratorium Period Works in Real Life?

Policies are easy to understand in theory. Reality is messier. Let’s break it down with a simple scenario:

You buy a policy in 2026. From year 1-5, insurers can investigate your disclosures. However, from year 9 onwards, there is limited ability to reject claims based on past non-disclosure

But there’s a catch: Continuity matters.

If you miss a renewal, let the policy lapse and restart later, the clock resets. That’s where many people slip. Imagine paying premiums for seven years, then forgetting one renewal due date. You revive the policy later, but you’re back to year zero of the moratorium.

Moratorium Period vs Waiting Period

These two terms often get mixed up. They are not the same.

|

Feature |

Moratorium Period |

Waiting Period |

|

Duration |

5 years (fixed by IRDAI) |

Varies (30 days to 3 years for pre-existing diseases as per IRDAI norms) |

|

Purpose |

Limits insurer's right to reject claims |

Delays when coverage begins |

|

Applies To |

Non-disclosure and misrepresentation |

Specific illnesses or conditions |

|

Starts From |

Policy inception |

Policy inception |

|

Best For |

Long-term policyholders |

New policy buyers |

Note: Policy terms vary by insurer and IRDAI updates. Always check current wording.

Think of it this way. Waiting periods control when you can claim. Moratorium periods control whether your claim can be challenged later. Both matter but in different ways.

What Changes After the Moratorium Period Ends?

The shift after 5 years is subtle but powerful. Before the moratorium ends, insurers can:

- Investigate past medical disclosures

- Reject claims if they find non-disclosure

- Re-examine your application details

After it ends:

- Claims cannot be rejected for non-disclosure (except fraud)

- Your policy becomes more stable

- The burden shifts away from you

That stability is the real value. Here’s a question worth asking yourself. Would you rather argue over paperwork during a medical emergency… or know your policy is locked in? That’s the difference.

Important Note: Fraud is treated differently. If an insurer proves deliberate fraud, they can still deny claims even after the moratorium period.

Diseases, Disclosures and the Grey Areas

Insurance is not always black and white. Consider this: you had mild hypertension before buying a policy but didn’t mention it. Five years later, you need treatment related to it. If the moratorium period is complete and there’s no fraud, your claim should stand. But what counts as fraud?

- Fabricated documents

- Fake medical records

- Intentional hiding of major conditions

Small omissions due to lack of awareness often fall into a grey zone. And that’s where the moratorium offers protection. Still, relying on that safety net isn’t wise. Honest disclosure upfront keeps things clean.

Also Read;

Costs, Premiums and Why Time Works in Your Favour

Remember, premiums don’t directly change because of the moratorium period. But its impact grows over time. A 30-year-old buying Rs. 10 lakh cover might pay Rs. 8,000-Rs. 12,000 annually. At 40, the same cover could cost Rs. 15,000-Rs. 25,000. At 50, premiums often cross Rs. 30,000.

Now add the moratorium angle. If you buy early and stay consistent, by your late 30s or early 40s:

- Your moratorium period is complete

- Your premiums are still relatively low

- Your policy is more secure

That combination is powerful. The numbers tell a different story. Delaying purchase means higher premiums and a delayed moratorium completion.

Recent IRDAI Updates (2024–2026)

- Moratorium period reduced from 8 years to 5 years

- Faster claim certainty due to earlier lock-in

- Greater focus on transparency and disclosures

Situations Where the Moratorium Period Becomes Critical

Most people don’t think about this clause until something goes wrong. Here are three moments where it matters most:

- Large Claims After Several Years

Hospital bills can easily cross Rs. 5-10 lakh. Insurers scrutinise big claims more closely, especially within the first 5 years.

- Pre-existing Conditions

Even if waiting periods are over, disclosure issues can still affect claims until the moratorium ends.

- Policy Porting

Switching insurers? Your continuity matters. If done correctly, your moratorium period continues. If not, it resets.

How to Maintain Continuity Without Resetting the Moratorium?

This part is practical. Small mistakes here cost years.

- Renew Before Due Date: Every policy has a grace period, usually 15-30 days. Missing even that can break continuity.

- Avoid Long Breaks: If a policy lapses and is later revived, insurers may treat it as a fresh start for moratorium calculation.

- Port, Don’t Replace: Use the official portability process when you want to change the insurer. Apply at least 45 days before renewal

- Provide medical history: Ensure continuity benefits are confirmed

- Keep Documentation Safe: Old policy documents matter. They prove continuity.

How to Port Your Health Insurance Without Losing Moratorium Benefits?

Switching insurers is common now. Done right, you carry your benefits forward.

- Initiate Porting Request Early

Visit your insurer’s website. Start at least 45 days before renewal. Late requests may get rejected.

- Submit Required Documents

You’ll need: -

- Previous policy copies

- Claim history

- ID proof

- Proposal form

Incomplete documents delay approval.

- Undergo Medical Evaluation (if required)

Insurers may ask for tests and their results can also affect acceptance terms.

- Wait for Approval Timeline

Insurers must respond within 15 days. If the insurer does not respond within the prescribed timeline, the request may be treated as deemed acceptance as per IRDAI portability guidelines.

- Confirm Continuity Benefits

Before paying the premium, check: -

- Waiting periods carried forward

- Moratorium continuity intact

Miss this step and you risk resetting your benefits.

- Pay Premium Before Deadline

Delays cancel the porting process. You may need to start again.

Common Misunderstandings About the Moratorium Period

Let’s clear a few myths:

|

"After 5 years, everything is covered" |

Not quite. Policy exclusions still apply. Cosmetic procedures or non-covered treatments remain excluded. |

|

"I don't need to disclose medical history" |

This is a wrong approach as fraud can override moratorium protections. |

|

"It applies separately to each illness" |

No, it applies to the policy as a whole, not individual diseases. |

|

"Switching insurers resets everything" |

Only if done incorrectly. Proper porting preserves continuity. |

How Insurers View Risk Over Time?

Insurers don’t just look at age or illness. They look at behaviour. A policyholder who renews on time, makes transparent disclosures and maintains continuity is considered low-risk over time.

That’s why the moratorium period exists. It rewards consistency. There’s a mild irony here. The longer you stay with a policy, the less scrutiny you face.

Must-Read Guides From SMC

Summing Up,

The moratorium period in health insurance quietly strengthens your policy over time. Five years of continuous coverage can turn a fragile contract into a far more dependable safety net. Buy early, renew without breaks and disclose honestly. That’s the path.

If you’re just starting, focus on choosing the right policy and staying consistent. If you already have a policy, protect its continuity like it matters. Because it does.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

FAQs

It is a 5-year period defined by IRDAI during which insurers can question claims based on non-disclosure. After this period, they cannot reject claims for such reasons unless fraud is proven.

Yes, IRDAI mandates this clause across health insurance policies in India, though wording may vary slightly by insurer.

Missing renewal beyond the grace period breaks continuity. The moratorium period may reset, depending on insurer rules.

No, waiting periods delay coverage for specific illnesses. The moratorium period limits claim rejection rights after 5 years.

They can only reject claims if they prove fraud. Non-disclosure alone is not enough after 5 continuous years.

Proper porting preserves continuity, including moratorium benefits. Buying a fresh policy resets the 5-year clock.

Yes, the moratorium applies separately to the increased portion from the date of enhancement.