Visit the SMC Insurance Brokers Official website and click on the “View All” option..

Time Remaining to Avail Tax Benefits

(Under section 80C & 80D)

Get 90 Lakh Health Cover at Just ₹2K

Buy Life Insurance Now!

100% Privacy

Zero Spam

Network

30+ Reliable Insurers

Legacy

20+ Years & Counting

Highly rated insurance website

4.1/5

Plans start at Just ₹30.79/day

Businesses rule India. And as a part of daily business life, commercial vans do play a very important role. They leave early, return late and spend most of their time on the road. From moving goods to transporting staff, they support work that runs on schedules and commitments. When a van is delayed or damaged, the effect is too big. Deliveries get delayed and services pause. This means that your costs begin to rise.

When a tractor stops working, work stops. Income gets delayed. Repair costs can hit savings hard. One accident, one fire, or one theft incident can create a financial problem that takes months or years to recover from. That is where tractor insurance plays a role. It protects tractor owners from large, sudden expenses that come from damage, accidents, or legal claims.

How about we explain commercial van insurance in a clear and practical way?

Commercial van insurance is a motor insurance policy created specifically for vans used for business purposes. They are different from private cars and usually travel longer distances, carry goods or passengers. And it goes without saying that they operate on tight schedules.

Because of this higher exposure, commercial vehicle insurance policies are meant to address business-related risks. They provide financial support if the van is damaged, stolen, or involved in an incident that causes harm to others.

A commercial van insurance policy helps cover repair costs, replacement costs and legal liabilities arising from daily vehicle use. It also ensures that the vehicle remains legally compliant under Indian motor laws.

Indian law requires every motor vehicle on the road to have at least third-party insurance. This applies to commercial vans as well. Third-party insurance protects other people on the road. If your van causes injury, death, or property damage, the policy helps cover compensation and legal expenses.

Without valid insurance, business owners may face fines, penalties and legal action. In serious cases, vehicles can be seized. Beyond legal issues, uninsured losses can disrupt operations and drain business funds.

And yes, commercial vehicle insurance is a financial safeguard for business continuity.

Commercial van insurance is required for anyone using a van to earn income or support business activity. This includes:

If a van is registered as a commercial vehicle or used regularly for work, personal car insurance is not enough. A commercial policy is required.

Commercial van insurance policies are mainly available in two forms. Each serves a different level of protection.

Knowing exclusions helps avoid claim rejection.

Add-ons allow businesses to extend coverage based on specific needs. They increase the premium slightly but offer better protection.

This add-on removes depreciation deductions during claim settlement. Without it, insurers reduce claim payout based on vehicle age and part wear. Zero depreciation is useful for newer vans and frequent repairs.

Engine damage due to water ingress or oil leakage is usually not covered under standard policies. This add-on protects the engine, especially useful in flood-prone areas.

Roadside assistance provides help during breakdowns. Services may include towing, battery jumpstart, fuel delivery and minor repairs. This helps reduce downtime during work hours.

No Claim Bonus reduces premium during renewal if no claims are made. This add-on protects the bonus even after a claim.

Consumables like nuts, bolts, lubricants and brake oil are usually excluded from standard claims. This add-on covers these small but frequent costs.

Insurance premium is calculated based on several factors related to risk and vehicle usage.

|

Vehicle Age and Model |

Newer vans usually cost more to insure due to higher value. Older vans may have lower premiums but fewer add-on options. |

|

Engine Capacity and Load Capacity |

Vans with higher engine power or load capacity face higher risk and often attract higher premiums. |

|

Usage Pattern |

Daily long-distance use increases exposure to accidents and wear. Premiums are higher for vans used frequently for deliveries or transport. |

|

Location of Operation |

Vehicles operating in high-traffic cities or theft-prone areas may have higher premiums. |

|

Claim History |

A clean claim history helps reduce renewal premium through no claim bonus benefits. |

|

Add-Ons Selected |

Each add-on increases premium but also improves coverage. Choosing only necessary add-ons helps control cost. |

Choosing the right policy depends on business usage, vehicle age and risk exposure. Before selecting a plan, consider:

For vans critical to daily revenue, comprehensive coverage with essential add-ons offers better long-term security.

Many businesses face issues due to avoidable mistakes:

Avoiding these helps maintain continuous and effective protection.

Renewing commercial van insurance on time is very important for any business that depends on vehicle movement. A policy usually stays valid for one year. Once it expires, the van is no longer protected. This creates legal risk and financial risk at the same time.

If a van runs on the road with an expired policy, penalties can apply under motor vehicle rules. Apart from fines, there is also a bigger concern. Any accident or damage during this period must be paid fully by the owner. For businesses, this can lead to sudden and heavy expenses.

Renewal is not only about staying legally safe. It also keeps coverage active without gaps. Continuous coverage helps maintain policy benefits like No Claim Bonus. This bonus lowers premium during renewal if no claims were made in the previous policy period. If the policy expires and is not renewed within the allowed grace window, this bonus may be lost.

Many insurers provide a short grace period after expiry. During this time, renewal is still possible. But coverage is usually not active during the gap. If an incident happens during this break, the insurer may not accept the claim. Because of this, renewing before expiry is always safer.

Timely renewal also helps avoid vehicle inspection. If a policy lapses for too long, insurers may ask for vehicle inspection before issuing a new policy. This can delay coverage and create operational issues, especially for businesses that use vans daily.

Usually required documents include:

Most insurers now support digital document submission.

Buying Commercial Van Insurance Online

Online platforms have simplified the buying process. Typical steps include:

Online purchase saves time and allows easy comparison.

Choosing the right commercial van insurance can be confusing due to multiple insurers and complex terms. SMC Insurance works as a platform that brings plans from leading insurers together. Businesses can compare options, understand coverage and choose a policy that matches real usage. Support includes:

The focus remains on clarity, not pressure.

When something goes wrong, the claim process becomes the most important part of your insurance policy. A well-managed claim can reduce downtime, control repair costs and help your business get back on track faster. A poorly handled claim can lead to delays, extra expenses, or rejection.

For commercial vans, claims often happen during work hours, while carrying goods or transporting staff. This makes speed and accuracy very important. The goal is simple. Inform early, document clearly and follow the insurer process step by step.

Most insurers allow claim intimation through call centers, mobile apps, or websites.

If the insurer has network garages, using them can simplify billing and reduce paperwork.

For commercial vehicles that must return to work quickly, this can be very useful.

Beyond immediate protection, insurance supports long-term business stability. It helps:

Insurance becomes part of risk management rather than an expense.

Getting commercial vehicle insurance through SMC’s website is quick and straightforward:

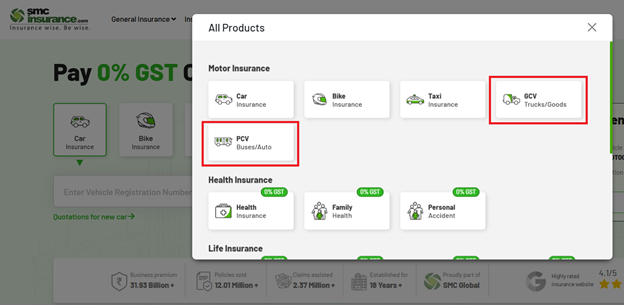

From the available options, select if your vehicle is GCV (Goods Carrying Vehicle) or PCV (Passenger Carrying Vehicle)

Once chosen, you will be taken to the respective page. You can use the on-screen widget and enter your vehicle number and click on “View Quotes”. This will directly take you to the commercial insurance buying process of SMC Insurance.

Fill in the required vehicle details. This includes vehicle category, brand, model, RTO location, and how long you want the policy to last.

Review quotes from multiple insurance partners and compare pricing and benefits side by side.

Customize your policy by adding optional protections like roadside support or engine cover, based on your needs.

Complete the payment online. Your policy documents are sent to your email soon after payment confirmation.

Download the policy from the SMC app or your email. Check all details carefully, then you’re set to drive with coverage in place.

In India, a commercial van is a working asset that supports income, service delivery and business growth. Commercial van insurance protects this asset against risks that cannot be predicted or controlled. From accidents to legal claims, insurance helps businesses stay prepared and financially secure.

With the right policy, businesses can operate confidently, knowing that unexpected events will not bring operations to a halt.

Disclaimer:The information provided on this platform is intended for general awareness and educational purposes. While every effort is made to ensure accuracy, some details may change with policy updates, regulatory revisions, or insurer-specific modifications. Readers should verify current terms and conditions directly with relevant insurers or through professional consultation before making any decision.

All views and analyses presented are based on publicly available data, internal research, and other sources considered reliable at the time of writing. These do not constitute professional advice, recommendations, or guarantees of any product’s performance. Readers are encouraged to assess the information independently and seek qualified guidance suited to their individual requirements. Customers are advised to review official sales brochures, policy documents, and disclosures before proceeding with any purchase or commitment.

(Showing Newest to Oldest)

Simple Process

The company is wonderful insurance platform providing multiple policies under 1 roof. Experience in purchasing the policy is very good. Experts guides you very well

Easy Renewal process

The process to renew my 2-wheeler policy is indeed very quick and easy. Got it done in just 10 minutes. Thanks.

Quick Response

I thought let me renew my two wheeler policy with SMC and see the experience. The experience was good and simple, the only gap which I felt was that the details of the vehicle did not come up after mentioning the vehicle number.

Yes, under the Motor Vehicles Act, all commercial vehicles must have at least a Third-Party Liability insurance policy to operate legally on public roads. This covers legal liabilities for injuries or damages caused to others. Comprehensive coverage, which includes protection for your own vehicle, is optional but recommended .

You can obtain quotes by visiting the SMC Insurance website. By entering your vehicle details, you can compare premiums and coverage options. It's advisable to compare multiple quotes to find the best fit for your needs .

You can purchase insurance directly from an insurer’s website, through a licensed broker, or via aggregator platforms. The process typically involves entering your vehicle and personal details, selecting coverage options, and making an online payment .

SMC Insurance allows policy renewal by entering your Vehicle Registration Number. The system retrieves your details, enabling you to compare and purchase policies without the need for a mobile login or OTP.

Passengers are covered if the policy includes specific add-ons for passenger liability. Standard Third-Party policies may not cover non-fare-paying passengers unless additional coverage is purchased .

Theft is covered under a Comprehensive or Package policy, which includes Own Damage coverage. Third-Party Liability policies do not cover theft .

Commonly recommended add-ons include:

To file a claim, you typically need:

Ensure all required documents are submitted promptly to facilitate the claim process

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

Tractor Insurance

Commercial Van Insurance

Passenger Carrying Vehicle Insurance

Goods Carrying Vehicle Insurance

PUC Rules For Commercial Vehicles

How To Renew Commercial Vehicle Insurance Online

Commercial Vehicle Insurance On EMI

Add-On Covers In Commercial Vehicle

RC Mismatch In Commercial Insurance

SMC Insurance Brokers Pvt. Ltd.

SMC Metro Mall, Near Pratap Nagar Metro Station, Pratap Nagar, New Delhi-110007

Registration No: 289, Registration Code No: IRDAI/DB-272/04/289, Valid till: 27/01/2029, License category: Composite Broker, CIN: U66000DL1995PTC172311

Insurance is the subject matter of solicitation.

Visitors are hereby informed that their information submitted on the website may be shared with insurers.

Product information is authentic and solely based on the information received from the Insurer.